BLOG - FINANCIA

From Oil Shock to Systemic Crisis: Global Markets Begin Repricing the Risk of Disruption

By mid-March 2026, the Iran conflict has moved beyond an energy shock: collapsing oil flows, attacks on infrastructure, and supply chain breakdowns are forcing financial markets to reprice not just commodities, but the stability of the global economic system itself.

FINANCIAL MARKETS

Mathéo Bockel

3/15/20263 min read

As of March 15, 2026, global financial markets are no longer reacting to a potential energy disruption, they are actively repricing the consequences of an unfolding systemic crisis. What began in late February as a geopolitical escalation has rapidly evolved into the largest disruption to global energy flows in modern history. Data from the International Energy Agency indicates that crude and refined product flows through the Strait of Hormuz, normally around 20 million barrels per day, have fallen to a fraction of their usual levels, effectively removing a critical share of global supply from accessible markets. At the same time, tanker traffic has nearly collapsed, with maritime transit through the strait dropping close to zero following repeated attacks on commercial vessels and escalating military threats. This is not simply a tightening of supply; it is a breakdown of the global energy logistics system.

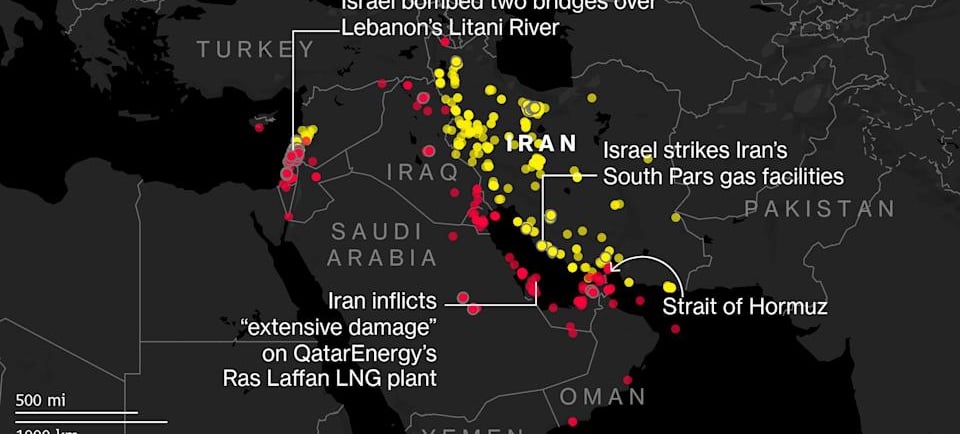

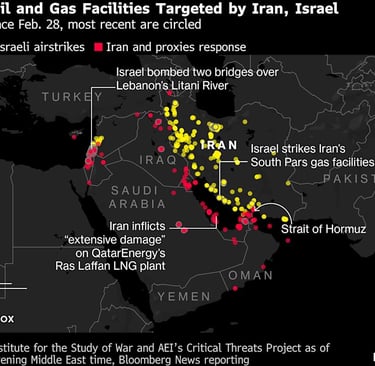

The escalation of military operations in early and mid-March has reinforced this dynamic. On March 13, U.S. forces conducted large-scale strikes on Kharg Island, Iran’s primary oil export hub, which handles up to 90% of the country’s exports, signaling a willingness to directly target the infrastructure underpinning global oil flows. Just days later, on March 18, major gas infrastructure at the South Pars field, responsible for a significant portion of Iran’s energy production, was hit, disrupting output and triggering immediate price reactions across global energy markets. In parallel, attacks on Saudi refining capacity, including the Ras Tanura facility, further destabilized supply chains and forced producers to reroute exports through less efficient channels. These developments confirm a critical shift: the conflict is no longer confined to geopolitical signaling, it is directly impairing the physical infrastructure of the global energy system.

Financial markets are responding accordingly, and the scale of the reaction reflects the systemic nature of the shock. Oil prices have surged beyond $100 per barrel, reaching levels not seen since the post-pandemic recovery, with peaks above $120 in some sessions as markets price both current disruption and the probability of further escalation. More importantly, the structure of the market itself is deteriorating: the gap between futures prices and the cost of physical fuel has widened significantly, reflecting acute shortages and logistical bottlenecks rather than purely financial speculation. This divergence is a key signal for investors, it indicates that markets are no longer functioning efficiently, and that access to physical supply has become a binding constraint.

Beyond energy markets, the shock is propagating rapidly across asset classes. Equity markets are beginning to reflect a classic risk-off regime, with major indices declining as investors reassess growth expectations and earnings visibility. At the same time, sectors are diverging sharply: energy producers and defense companies benefit from rising prices and geopolitical demand, while industrials, transportation, and consumer sectors face mounting cost pressures. Credit markets are also tightening, with widening spreads reflecting both higher inflation expectations and increased default risk in energy-sensitive industries. This is particularly relevant for leveraged structures, where rising input costs and interest rates combine to erode cash flow stability.

The macroeconomic implications are equally significant and increasingly visible. The disruption of energy flows through Hormuz, which accounts for roughly 20% of global oil and LNG supply, is generating cost-push inflation on a global scale, with direct effects on transportation, manufacturing, and food production. Analysts are already warning of the potential for a stagflationary environment, as rising costs coincide with slowing growth and declining trade volumes. In some regions, the impact is immediate and tangible: fuel shortages, rationing risks, and sharp increases in consumer prices are already being reported, highlighting the speed at which energy shocks translate into real economic stress. The release of more than 400 million barrels from strategic reserves by the International Energy Agency underscores the severity of the situation and the limited policy tools available to stabilize markets.

From an investment perspective, March 15 marks the transition from a volatility regime to a systemic repricing regime. The key shift is that markets are no longer pricing energy scarcity alone, they are pricing the probability of prolonged disruption. This has profound implications for capital allocation. Traditional leveraged buyout strategies become significantly more challenging, as higher interest rates, increased volatility, and reduced earnings visibility combine to raise the cost of capital and compress valuation multiples. At the same time, new opportunity sets are emerging, particularly in infrastructure, energy logistics, and distressed assets, where dislocation creates entry points for long-term investors.

Ultimately, the defining feature of this moment is conceptual. Financial markets are transitioning from a framework based on efficiency and globalization to one defined by fragmentation and uncertainty. The critical variable is no longer the price of oil itself, but the stability of the system that delivers it. In this context, resilience, whether in supply chains, energy sourcing, or capital structure, becomes a central determinant of value. March 15, 2026, therefore represents more than the peak of an energy crisis: it marks the point at which global finance begins to fully internalize the reality that geopolitical disruption is no longer a tail risk, but a core driver of market behavior.

GET IN TOUCH

Have a question, a partnership idea, or want to share your thoughts about finance?

At Financia, we value meaningful connections with our readers and collaborators.

Reach out and let’s start a conversation, your insights could inspire our next article.