BLOG - FINANCIA

Post-Recession Investing in April 2025: Where to Allocate Capital After Trump’s Tariff Shock

As of April 2025, in the aftermath of a tariff-driven recession, this article explores how to reposition a global portfolio. It analyzes the impact on equities, bonds, gold and currencies, and outlines practical multi-asset allocation strategies for different risk profiles.

PORTFOLIO MANAGEMENT

Mathéo Bockel

4/15/20252 min read

Macro Context (April 2025 - Essentials)

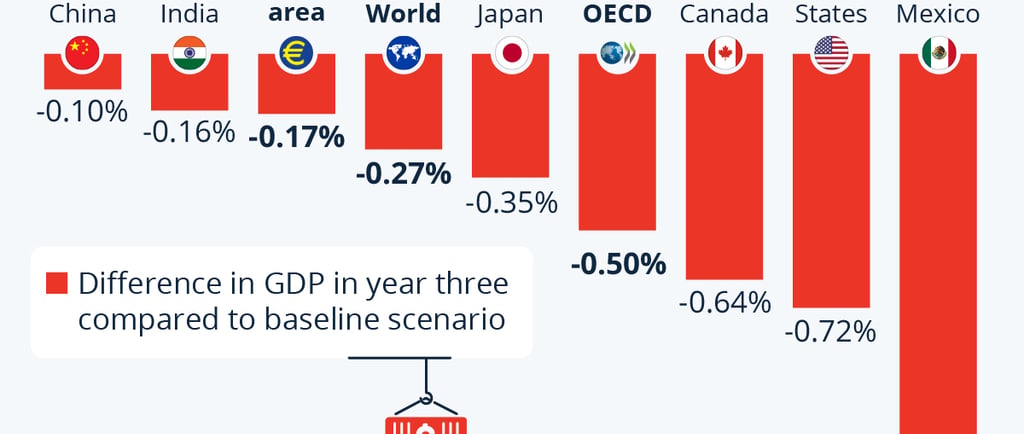

The global economy entered a technical recession in late 2024, triggered by a sharp escalation in US trade tariffs under Donald Trump’s protectionist agenda. Broad import duties led to:

Supply chain disruptions

Cost-push inflation

Collapsing business confidence

A synchronized slowdown in global trade

By Q1 2025, recessionary dynamics peaked. As of April 2025, markets are transitioning into a fragile recovery phase, supported by:

Monetary easing from the Federal Reserve

Fiscal stimulus in Europe and Asia

Partial normalization of global trade flows

This regime favors selective risk-taking, not broad beta exposure.

Asset Allocation Priorities for 2025

Gold & Precious Metals (Core Allocation)

Rationale

Persistent geopolitical risk

Structural inflation uncertainty

Central bank reserve diversification

Falling real interest rates

Gold remains a strategic anchor in portfolios post-recession.

Allocation guide:

7–12% of a diversified portfolio

Sources: World Gold Council, IMF reserve data, Bloomberg

Defensive & Quality Equities (Selective Risk)

Favored sectors

Healthcare

Utilities

Defense & cybersecurity

Infrastructure

Why

Pricing power

Stable cash flows

Lower sensitivity to trade shocks

Geographic preference

US large caps (domestic demand bias)

Japan (yen weakness + corporate reform)

India & ASEAN (structural growth, less tariff exposure)

Avoid

Export-heavy cyclicals

Highly leveraged industrials

Sources: MSCI, BlackRock Investment Institute, OECD

Bonds: Duration Is Back

Post-recession signal

Peak inflation behind us

Central banks shifting from restrictive to accommodative stance

Best opportunities

US Treasuries (intermediate duration)

Investment Grade corporate bonds

Select sovereign debt (core Europe)

Avoid

High-yield credit (default risk lagging indicator)

Sources: Federal Reserve, ECB, Moody’s

Energy & Strategic Commodities (Tactical)

Focus

Oil (geopolitical risk premium)

Uranium (energy security)

Copper (long-term electrification)

These assets hedge re-inflation risk during recovery.

Allocation: Tactical (5–8%)

Sources: IEA, World Bank Commodity Outlook

Cash & Liquidity (Optional Dry Powder)

Volatility remains elevated post-recession. Holding cash:

Preserves optionality

Enables tactical re-entry on market stress

Allocation: 5–10% depending on risk profile

What to Avoid in 2025 for the moment

Over-leveraged growth stocks

Pure globalization plays

Emerging markets highly dependent on US trade

Speculative crypto assets (liquidity-sensitive)

Model Portfolio for the moment (April 2025 - Balanced Profile)

Asset ClassAllocationEquities (Defensive + Quality) 35%

Bonds (IG + Sovereigns) Gold 30% & Precious Metals 10%

Commodities 10%

Cash 10%

Alternatives 5%

Strategic Takeaway

The post-tariff recession environment of 2025 is not a return to pre-2020 globalization. It marks a regime shift toward:

Higher geopolitical risk

Structural inflation volatility

Fragmented trade blocs

Successful portfolio management in 2025 requires:

Resilience over momentum, quality over leverage, and diversification over concentration.

Key Sources

IMF · World Gold Council · Federal Reserve · ECB · World Bank · OECD · BlackRock Investment Institute · Bloomberg

GET IN TOUCH

Have a question, a partnership idea, or want to share your thoughts about finance?

At Financia, we value meaningful connections with our readers and collaborators.

Reach out and let’s start a conversation, your insights could inspire our next article.